The market has found its latest AI casualty: the outsourced customer operations sector.

Amid recent pressure on major BPO stocks, a familiar narrative has taken hold. We are told that generative AI and agentic automation are coming for the human agent. Volumes will fall. Seats will disappear. Revenues will compress. The old outsourcing model will be dismantled by software.

There is truth to that story, but it is not the whole truth.

The market is right to question the traditional BPO model. It is wrong to assume that outsourced customer experience has no future. What AI is really exposing is not the irrelevance of BPO, but the fragility of a commercial model built too heavily on headcount, seat count and labour arbitrage.

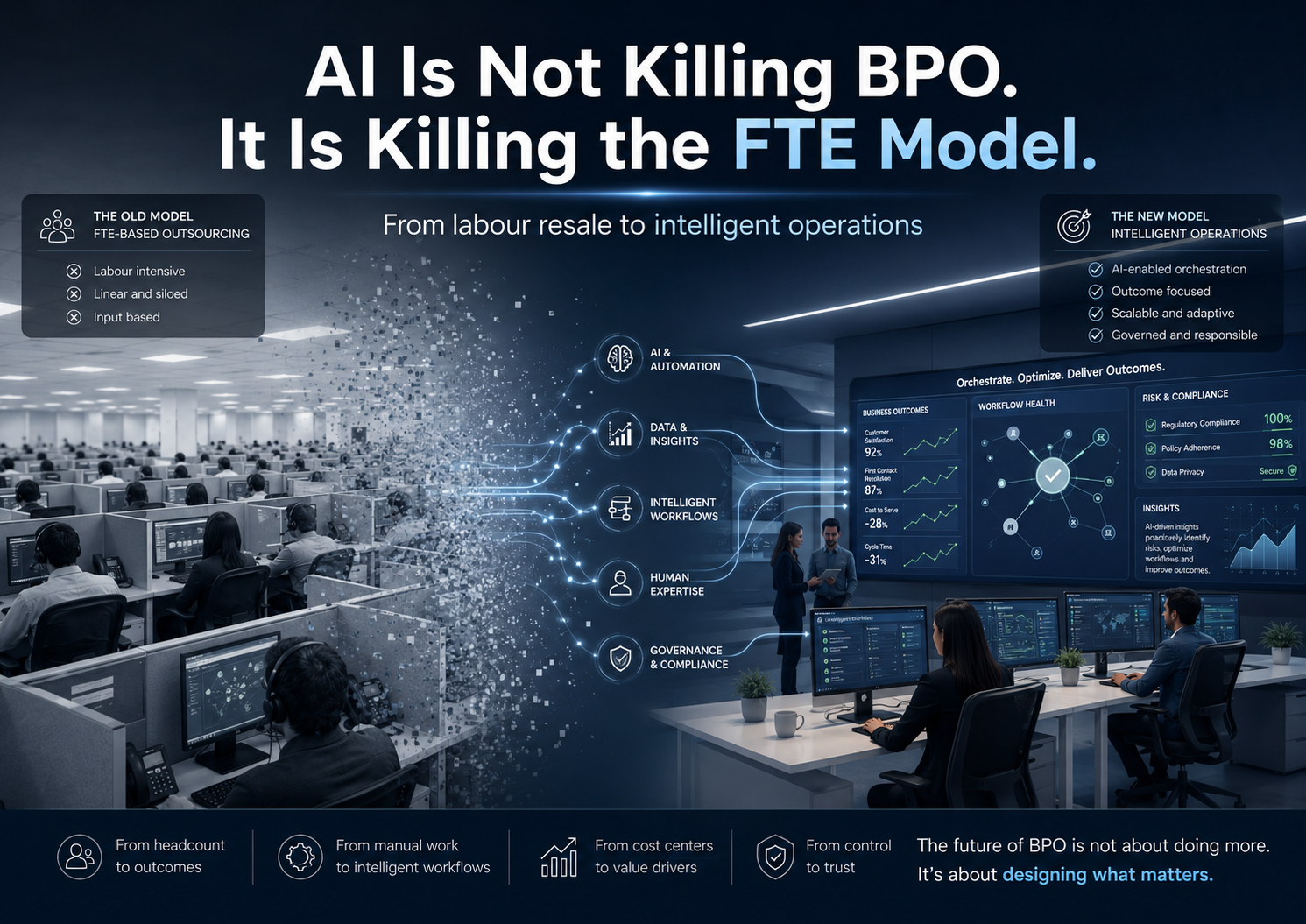

AI is not killing BPO. It is killing BPO as an FTE-resale business.

The old equation is breaking

For decades, much of the outsourcing industry was built on a simple equation: more volume meant more people; more people meant more revenue; cheaper locations meant better economics.

That model was powerful when customer operations were labour-intensive, process-heavy and difficult to automate. It gave enterprises scale, flexibility and a cost advantage. It gave providers a predictable commercial engine. But it also created a structural dependency: revenue growth became too closely tied to human capacity.

AI changes that equation.

When customer intent can be recognized automatically, simple queries can be resolved through self-service, agents can be augmented in real time, quality assurance can move from sample-based review to full-interaction analytics, and back-office work can be redesigned around workflow intelligence, the traditional unit of value begins to shift.

The question is no longer simply “How many people do we need?”

It becomes, “How much work can be intelligently resolved, routed, augmented, assured, or redesigned?”

That is a very different kind of business.

The market reaction is not irrational

It would be a mistake to dismiss recent investor concern as panic. The pressure is real.

Concentrix reported modest Q2 growth, lower non-GAAP operating income and revised full-year guidance, while emphasizing momentum in AI-enabled solutions and its blended AI-and-services approach. Teleperformance reported a soft Q1, with group revenue down on both a reported and like-for-like basis, and highlighted automation trends, offshore delivery momentum and slower ramp-ups in parts of the business.

These are not imaginary pressures. They signal that a sector is in transition.

Some low-complexity work will be automated. Some activities will move offshore. Some clients will use AI to reduce volumes. Some contracts will be renegotiated. Some legacy revenue will not return in the same form.

The mistake is not in recognizing the pressure. The mistake is in assuming that the decline of the old model is the same as the sector’s death.

Demand is not disappearing. It is migrating.

Enterprises still have customers. They still face complaints, claims, payments, onboarding journeys, sales conversations, service failures, regulatory obligations and emotionally charged moments of truth. They still need operational resilience, multilingual support, compliance, workforce flexibility and specialist judgement.

What is changing is the nature of the work.

The future of BPO will not be defined by armies of agents handling repetitive transactions. It will be defined by the ability to orchestrate complex service systems in which AI, human expertise, data, workflow, compliance and customer experience converge.

That is why the most interesting signals from the sector are not only the revenue figures. They are the strategic responses.

Concentrix is positioning itself around intelligent operations: designing, building and running systems that connect people, AI and technology. Teleperformance is explicit about rewiring its core, reshaping the business, developing AI-powered offerings, strengthening its AI leadership and doubling down on outcome-based deals across sales, collections and back-office solutions.

This is the real story. The industry is not simply trying to protect the old call-centre model. The leading players are trying to reinvent the operating model underpinning it.

The new value sits in orchestration

The simplistic version of the AI story says that the agent is replaced by a bot.

The enterprise reality is more complex.

AI may handle serviceable intents. Human agents may handle complex, high-value or emotionally sensitive interactions. Automated systems may triage, summarise and recommend. Human specialists may intervene where judgement, empathy, escalation or accountability are required. Quality assurance may become continuous. Data may become the operating layer. Compliance may need to be engineered into the workflow rather than checked after the fact.

This is not substitution. It is system redesign.

Teleperformance’s own materials describe AI agents handling serviceable intents, while human agents support more complex, higher-value, and higher-emotional-load interactions, with both integrated with enterprise systems and sector-specific workflows. That is a much more useful picture of the future than the crude “AI versus humans” framing.

The next-generation provider will not merely supply labour. It will help clients determine which work should be automated, which should be augmented, which should remain human, which should be redesigned, and how the whole system should be governed.

That is where value migrates: from bodies to orchestration.

The commercial model must change

This transition poses a serious challenge for BPO providers.

If revenue remains tied to FTEs, AI poses a commercial threat. Every automated interaction looks like lost income. Every productivity gain creates commercial tension. Every client transformation becomes a margin problem.

That is why the pricing model must evolve.

The next phase of BPO cannot be built solely on seats, hours and volumes. It will need more outcome-based models, gain-share mechanisms, transformation fees, platform-enabled services, managed AI operations, governance services and continuous optimization.

In other words, providers need to be paid for the value they create, not just the labour they deploy.

That is easier said than done. It requires new sales models, new contracting structures, new delivery capabilities, new technology partnerships, new risk controls and new management disciplines. It also requires clients to stop treating BPO as a procurement category and to start treating it as part of enterprise operating model design.

This is the difficult middle of the transition. Legacy revenues are under pressure before new models have fully scaled. Providers must fund transformation while defending margins. Clients want savings, but also resilience. AI promises productivity but introduces new governance, integration and accountability demands.

That is why the sector is being repriced. However, repricing is not the same as obsolescence.

The winners will redesign the work

The winners in the next phase will not be the providers that simply defend their seats. Nor will they be the enterprises that assume they can buy AI tools and switch off outsourced operations overnight.

The winners will be those who redesign the work.

They will understand customer journeys at the level of intent, emotion, risk and value. They will know where automation genuinely improves the experience and where it simply transfers frustration. They will integrate AI into live operations rather than treating it as a bolt-on. They will embed governance within the operating model. They will apply human expertise where it matters most. They will measure outcomes, not activity.

For enterprises, the strategic question is no longer whether AI will reduce headcount. In many areas, it will. The better question is whether the organization has the operating model, data, governance, technology and partner ecosystem to turn that reduction into improved performance.

For BPO providers, the question is equally stark. Are they still selling capacity, or are they becoming intelligent operations partners?

The market is sending a clear signal. The FTE model is losing its status as the default unit of value.

The future of BPO will not belong to those who can supply the most people at the lowest cost. It will belong to those who can orchestrate the best combination of AI, human judgement, workflow, data and accountability to deliver measurable outcomes.

AI is not killing BPO.

It is forcing BPO to become what it has always claimed to be: a transformation partner, not a labour broker.

Notes

- Concentrix Reports Second Quarter 2026 Results: https://ir.concentrix.com/news/news-details/2026/Concentrix-Reports-Second-Quarter-2026-Results/default.aspx

- Teleperformance First-quarter 2026 revenue: https://www.tp.com/media/51ob00no/tp-press-release-q1-2026-revenue.pdf